Scan barcode

rick2's review against another edition

5.0

Lo puts into words so many things I have been trying to piece together. Reading the first chapter felt like finding your car keys after a desperate, brain wracking search. Finally someone taking a robust multidisciplinary approach to finance. Lo combines a variety of sources from psychology, neuroscience, evolutionary theory, organizational theory, finance, history and biology to create his theory of Adaptive Markets. Until this, I had all but given up on economists as stodgy old coots trying to chart nonsensical metrics. Or as statisticians who won't leave their ivory towers for fear that it may ruin their "perfect" models. While I don't believe the Adaptive Markets hypothesis Lo proposes is the ultimate answer to the EMH, it is the best contender I have read to date.

However, if we are going to ascribe biological traits to markets, market participants seem more akin to simple single celled organisms. For all of the technological horsepower at hedge funds and quant shops, they still operate more like ravenous microorganisms, not the high level predators and herbivores Lo imagines. Lo appears to miss the filter produced through the difficulty in codifying and producing an investment strategy. And sadly, despite his use of complex graphs and plots, technology is not a topic he fundamentally seems to incorporate into this hypothesis beyond its applications as a magic bullet. (See references to Moore’s law) In this book technology’s impact seems more like an afterthought. As are the regulatory suggestions he offers. Note that none of this negates Lo’s core ideas, but are merely issues I think have not yet been fully thought out.

Overall, reading this book gives me hope that there are still those in economics who are using their brains instead of just their spreadsheets.

However, if we are going to ascribe biological traits to markets, market participants seem more akin to simple single celled organisms. For all of the technological horsepower at hedge funds and quant shops, they still operate more like ravenous microorganisms, not the high level predators and herbivores Lo imagines. Lo appears to miss the filter produced through the difficulty in codifying and producing an investment strategy. And sadly, despite his use of complex graphs and plots, technology is not a topic he fundamentally seems to incorporate into this hypothesis beyond its applications as a magic bullet. (See references to Moore’s law) In this book technology’s impact seems more like an afterthought. As are the regulatory suggestions he offers. Note that none of this negates Lo’s core ideas, but are merely issues I think have not yet been fully thought out.

Overall, reading this book gives me hope that there are still those in economics who are using their brains instead of just their spreadsheets.

mbidanda's review against another edition

5.0

Cool theory. Fun behavioral journey to get there. Lets hope academia allows this idea to continue to evolve ...

bulletobinary's review

5.0

This book beautifully wove together psychological research and the evolution of the financial market. Breaking down neuropsychological factors into understandable chunks as they relate to financial decision making and then weaving it into the growing technology of trading and the speed at which this technology changes the markets and then sprinkling in all the rules, regulations, and strategies, ugh, this book is PRICELESS for anyone who wants to learn about the financial world as it relates to being imperfect and controlled by human factors. It's basically like if Robert Sapolsky were an economist.

joaoveloso's review

4.0

This book is more of a constructive argument for the need of new perspective in finance, investing and how markets work in general than about how markets work.

It shines some light on each bit of the financial institutions, however it is too sparse in my opinion.

Overall it's a good read, but different from what I expected

It shines some light on each bit of the financial institutions, however it is too sparse in my opinion.

Overall it's a good read, but different from what I expected

yeconomist's review

5.0

I found this book to be exceptional. This book brought together a multitude of different disciplines and approaches in crafting a well argued challenge to orthodox economic thinking. In particular, as Lo notes, it takes a theory to beat a theory and the adaptive market hypothesis which he has proposed is a noble contender to the highly lauded efficient market hypothesis.

The narrative that Lo crafts, an exposition on the power of narratives generally, does an effective job in tying together what seem to be disparate lines drawn from psychology, sociology, finance, biology and economics, among others. As a relative expert in one of these fields and more of a casual observer of the others I found Lo did an amazing job in writing at a level that was easy enough to follow for the uninitiated and not boring for the knowledgable. Lo mainly limiting the discussion of details to those that seemed fundamental to understanding the specific arguments being made, so as not to get marred by unnecessary technical discussions/distinctions. Moreover, the interspersion of the scientific and academic findings and results with a discussion of the lives of the scientists and academics involved made the book much more engaging and easy to follow along with. This also did an effective job in setting the scene for what was going on in the wider world furthering this idea that environment, at both large and small scales, matters.

Beyond learning about these different fields, an important value add by this book is the structural lens it provides with which to think about the world. While many of the scientific findings discussed the author are discussed elsewhere, when packaged together they create a valuable perspective from which to approach future problems. In particular, thinking about things in terms of the ecosystem and the different actors involved and how the incentives shape interactions. In addition, the notion that you should constantly test your assumptions will be a valuable consideration when thinking about any kind of system, be it a household, workplace or financial markets. The ruthless assault on the standard economic assumptions was also well articulated and did a good job of challenging my own preconceived notions of how humans act in the real world, adding a lot of colour.

Overall, this book was well written and helped to challenge my own biases on understanding human behaviour. It taught me a lot about the history of finance and financial economics as well as key results from the fields discussed above. Beyond the core science discussed I am confident that the ideas of adaption, the power of human innovation at the speed of thought and the optimism that was seeped throughout the book, though especially in the final chapter, was encouraging and will continue to be relevant to my life moving forward.

The narrative that Lo crafts, an exposition on the power of narratives generally, does an effective job in tying together what seem to be disparate lines drawn from psychology, sociology, finance, biology and economics, among others. As a relative expert in one of these fields and more of a casual observer of the others I found Lo did an amazing job in writing at a level that was easy enough to follow for the uninitiated and not boring for the knowledgable. Lo mainly limiting the discussion of details to those that seemed fundamental to understanding the specific arguments being made, so as not to get marred by unnecessary technical discussions/distinctions. Moreover, the interspersion of the scientific and academic findings and results with a discussion of the lives of the scientists and academics involved made the book much more engaging and easy to follow along with. This also did an effective job in setting the scene for what was going on in the wider world furthering this idea that environment, at both large and small scales, matters.

Beyond learning about these different fields, an important value add by this book is the structural lens it provides with which to think about the world. While many of the scientific findings discussed the author are discussed elsewhere, when packaged together they create a valuable perspective from which to approach future problems. In particular, thinking about things in terms of the ecosystem and the different actors involved and how the incentives shape interactions. In addition, the notion that you should constantly test your assumptions will be a valuable consideration when thinking about any kind of system, be it a household, workplace or financial markets. The ruthless assault on the standard economic assumptions was also well articulated and did a good job of challenging my own preconceived notions of how humans act in the real world, adding a lot of colour.

Overall, this book was well written and helped to challenge my own biases on understanding human behaviour. It taught me a lot about the history of finance and financial economics as well as key results from the fields discussed above. Beyond the core science discussed I am confident that the ideas of adaption, the power of human innovation at the speed of thought and the optimism that was seeped throughout the book, though especially in the final chapter, was encouraging and will continue to be relevant to my life moving forward.

wilte's review

4.0

I had very high expectations that were not completely fulfilled. The book feels a bit unorganised and a rambling collection of cool insights.

It also takes a while to get to the main point (the Adaptive Markets Hypothesis in Chapter 6, almost half way in the book). In the chapters before that we get an introduction to (behavioral) economics, and to the theory of evolution. Perhaps because of my background (evolutionary biologist working at a financial regulator), I did not read a lot of new things. Obviously financial markets and evolutionary theory are related...

Plenty of interesting stuff, though, and probably a good starter. Beinhocker's The Origin of Wealth: Evolution, Complexity, And the Radical Remaking of Economics (2006) is probably more in depth (but it is a while since I read that book, plus the financial world has been on a roler coaster since that book was published).

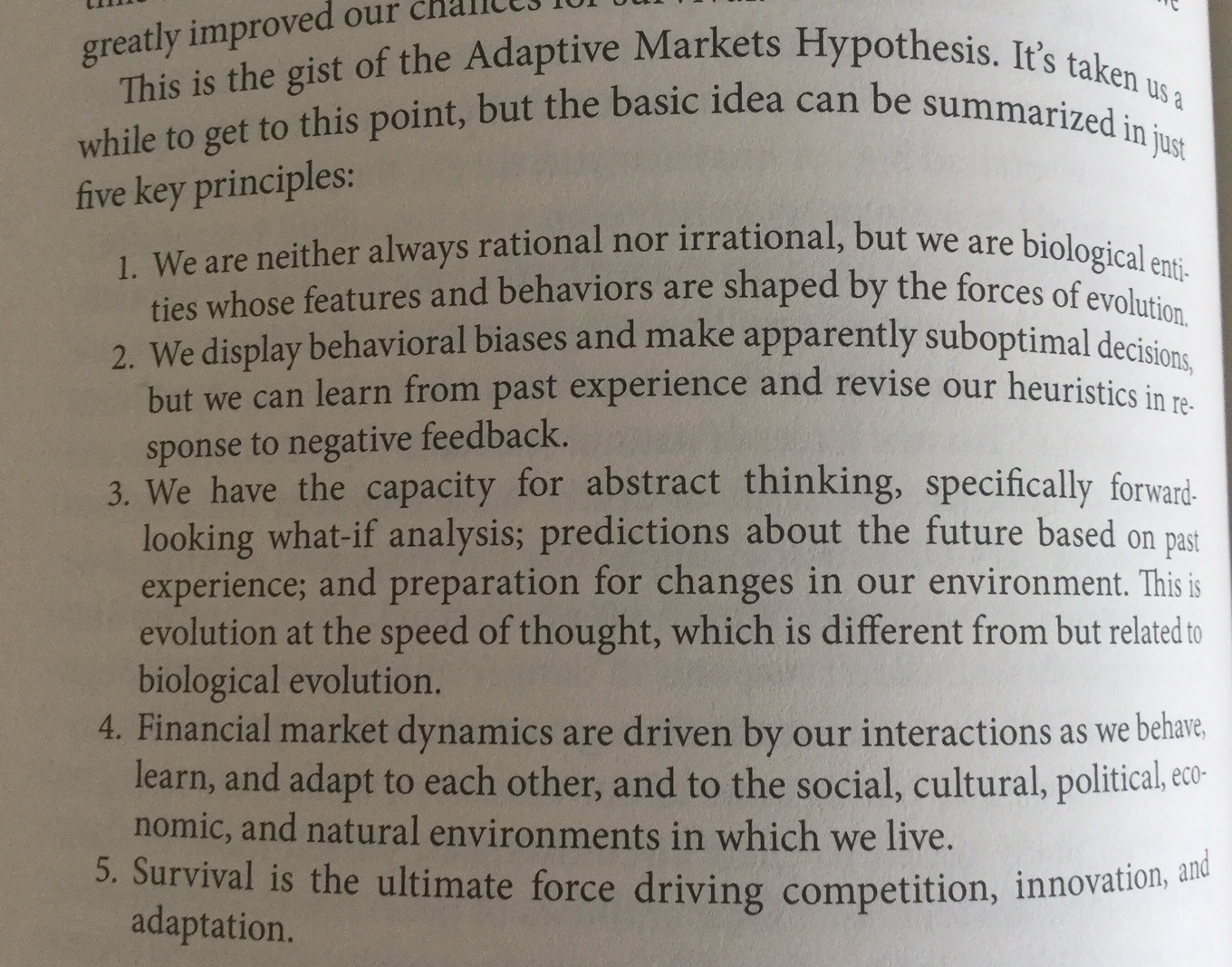

The Adaptive Markets Hypothesis is based on insight that financial markets behave more like biology than physics (p2). The Efficient Markets Hypothesis is not wrong, it is incomplete (p3). The wisdom of the crowds is sometimes overwhelmed by the madness of mobs. Lo introduces it, because it takes a theory to beat a theory. Incidently, John Boggle has the Costs Matter Hypothesis (p265).

p262: Under the AMH, risk isn't necessarily always rewarded, it depends on the environment.

p188:

However, even evolution at the speed of thought hasn't completely adapted to trading at the speed of light (p360).

Financial behavior that may seem irrational now is really behavior that hasn't had sufficient time to adapt to modern contexts (p9).

p189 (parafrased): Supotimal behavior is going to happen when we take heuristics (rules of thumb) out of the environment in which they emerged (evolved). Not "irrational" but "maladaptive".

Many behavioral biases are the result of our natural human tendency to forecast and plan ahead - but applied to the wrong environment (p66) We are short term demanding and long-term inattentive by nature (p99).

p103 Damasio: to be fully rational, we need emotion. When ability to experience emotions is removed, human behavior becomes less rational (p108; from Damasio (1994) Descartes' Error: Emotion, Reason and the Human Brain).

p117: Human is not a rational animal, but a rationalizing animal (Gazzaniga work).

EMH: Prices fully reflect all available information, markets crystallize the wisdom of crowds (p26).

Case in point is Maloney & J.H. Mulherin (2003) The Complexity of Price Discovery in an Efficient Market:The Stock Market Reaction to the Challenger Crash:

And Fama-paper (FFJR) The Adjustment of Stock Prices to New Information (1969): Stock prices jumped up on the day that a split was announced, but show no clear direction on the day the split actually occured (p24).

Fama used rule-of-thumb if asked to speak at an event: would I do it if it was next week? (contra hperbolic discounting) (p98).

A prediction market with N=28 students yielded STOC-rankings that correlated about 85% with traditional (extensive & expensive) consumer-survey rankings (Ely et al, 2008).

Frank Knight (1921) introduced useful distinction between risk (randomness that can be measured or quanitfied) and uncertainty (randomness that can't be measured or quanitfied) (p55).

p415: The Adaptive Markets Hypothesis tells us that as we transform uncertainty into risk (e.g. CancerCure bonds), investors will adapt and capital will follow.

Peltzman effect with data (p206): Professor Believes Safer Race Cars Result In More Accidents. New NASCAR safety measures led to more accidents (Sobel & Nesbit, 2007).

Selection works not only on our genes, but also on our social and cultural norms. (p207).

Three key features of the financial ecosystem (p332)

p327: In 2001 important change in the finacial ecosystem. Prior, stock prices/US exchanges moved in discrete units of $0.125. That was changed decimalization, so increments of $0.01. That led to more risk/less easy profits for market makers. ALso, hedge funds undercut market makers. Minor changes in financial environment like decimalization can lead to major changes in the ecosystem.

p354 Culture is very much a product of the environment, and as environments change, so does culture.

Lo is critical on the Israeli judges study (less parole right before lunch due to decision fatigue, p166). Rightly so probably, see e.g. Impossibly Hungry Judges. HOwever, he is quite so critical on the bankers' ethics/dishonesty study (see e.g. Bankers are more honest than the rest of us) or the Kerala fishermen using mobile phones to stabilize market prices (Surprise! Fishermen Using Mobile Phones for Market Prices is the Largest Lie in ICT4D). Perhaps those results are real, but there is some pushback.

p375: complexity of regulations, more interdependencies is more unstable.

Lo argues for something like National Transport Safety Board (NTSB) that -independent & transparant- investigates all (air traffic) accidents and has the whole sector learn from the findings.

Culture can be changed, by changing environment. But call it behavioral risk management (p388)

But: how to measure human behavior?

Eisenbach et al (NY Fed 2015) What Do Banking Supervisors Do?.

DNB (2009) The Seven Elements of an Ethical Culture Strategy and approach to behaviour and culture at financial institutions 2010-2014.

Parting words from Lo (p420): Financie doesn't have to be a zero-sum game if we don't let it.

About one third of variation in investment behavior is attributed to genetics; Barnea, Cronqvist, Siegel (2010)

Nature abhores an undiversified bet (p195) [i.e.: hedge risks most effectively]

Leibowitz (2005) Alpha Hunters and Beta Grazers

J. Doyne Farmer (2002) Market force, ecology and evolution

It also takes a while to get to the main point (the Adaptive Markets Hypothesis in Chapter 6, almost half way in the book). In the chapters before that we get an introduction to (behavioral) economics, and to the theory of evolution. Perhaps because of my background (evolutionary biologist working at a financial regulator), I did not read a lot of new things. Obviously financial markets and evolutionary theory are related...

Plenty of interesting stuff, though, and probably a good starter. Beinhocker's The Origin of Wealth: Evolution, Complexity, And the Radical Remaking of Economics (2006) is probably more in depth (but it is a while since I read that book, plus the financial world has been on a roler coaster since that book was published).

Adaptive Markets Hypothesis

The Adaptive Markets Hypothesis is based on insight that financial markets behave more like biology than physics (p2). The Efficient Markets Hypothesis is not wrong, it is incomplete (p3). The wisdom of the crowds is sometimes overwhelmed by the madness of mobs. Lo introduces it, because it takes a theory to beat a theory. Incidently, John Boggle has the Costs Matter Hypothesis (p265).

p262: Under the AMH, risk isn't necessarily always rewarded, it depends on the environment.

p188:

However, even evolution at the speed of thought hasn't completely adapted to trading at the speed of light (p360).

(ir)rational

Financial behavior that may seem irrational now is really behavior that hasn't had sufficient time to adapt to modern contexts (p9).

p189 (parafrased): Supotimal behavior is going to happen when we take heuristics (rules of thumb) out of the environment in which they emerged (evolved). Not "irrational" but "maladaptive".

Many behavioral biases are the result of our natural human tendency to forecast and plan ahead - but applied to the wrong environment (p66) We are short term demanding and long-term inattentive by nature (p99).

p103 Damasio: to be fully rational, we need emotion. When ability to experience emotions is removed, human behavior becomes less rational (p108; from Damasio (1994) Descartes' Error: Emotion, Reason and the Human Brain).

p117: Human is not a rational animal, but a rationalizing animal (Gazzaniga work).

Efficient markets?

EMH: Prices fully reflect all available information, markets crystallize the wisdom of crowds (p26).

Case in point is Maloney & J.H. Mulherin (2003) The Complexity of Price Discovery in an Efficient Market:The Stock Market Reaction to the Challenger Crash:

Within an hour, the market seems to have placed the blame for the crash on Morton Thiokol, the party ultimately judged by authorities to have been at fault. The firm’s one-day decline of 12 percent was quick, permanent, and reasonably corresponds to the subsequent losses in terms of legal liability, repair costs and lost future business.

And Fama-paper (FFJR) The Adjustment of Stock Prices to New Information (1969): Stock prices jumped up on the day that a split was announced, but show no clear direction on the day the split actually occured (p24).

Fama used rule-of-thumb if asked to speak at an event: would I do it if it was next week? (contra hperbolic discounting) (p98).

A prediction market with N=28 students yielded STOC-rankings that correlated about 85% with traditional (extensive & expensive) consumer-survey rankings (Ely et al, 2008).

Risk & uncertainty

Frank Knight (1921) introduced useful distinction between risk (randomness that can be measured or quanitfied) and uncertainty (randomness that can't be measured or quanitfied) (p55).

p415: The Adaptive Markets Hypothesis tells us that as we transform uncertainty into risk (e.g. CancerCure bonds), investors will adapt and capital will follow.

Selection

Peltzman effect with data (p206): Professor Believes Safer Race Cars Result In More Accidents. New NASCAR safety measures led to more accidents (Sobel & Nesbit, 2007).

Selection works not only on our genes, but also on our social and cultural norms. (p207).

Environment

Three key features of the financial ecosystem (p332)

- Behavior of different species (e.g. banks, hedge funds)

- The environment in which the behaviors take place

- How the two interact and evolve over time (G x E interactions in biology parlance)

p327: In 2001 important change in the finacial ecosystem. Prior, stock prices/US exchanges moved in discrete units of $0.125. That was changed decimalization, so increments of $0.01. That led to more risk/less easy profits for market makers. ALso, hedge funds undercut market makers. Minor changes in financial environment like decimalization can lead to major changes in the ecosystem.

p354 Culture is very much a product of the environment, and as environments change, so does culture.

Debunked?

Lo is critical on the Israeli judges study (less parole right before lunch due to decision fatigue, p166). Rightly so probably, see e.g. Impossibly Hungry Judges. HOwever, he is quite so critical on the bankers' ethics/dishonesty study (see e.g. Bankers are more honest than the rest of us) or the Kerala fishermen using mobile phones to stabilize market prices (Surprise! Fishermen Using Mobile Phones for Market Prices is the Largest Lie in ICT4D). Perhaps those results are real, but there is some pushback.

Regulators

p375: complexity of regulations, more interdependencies is more unstable.

Lo argues for something like National Transport Safety Board (NTSB) that -independent & transparant- investigates all (air traffic) accidents and has the whole sector learn from the findings.

Culture can be changed, by changing environment. But call it behavioral risk management (p388)

But: how to measure human behavior?

Eisenbach et al (NY Fed 2015) What Do Banking Supervisors Do?.

DNB (2009) The Seven Elements of an Ethical Culture Strategy and approach to behaviour and culture at financial institutions 2010-2014.

Parting words from Lo (p420): Financie doesn't have to be a zero-sum game if we don't let it.

Factoids/follow-up reading

About one third of variation in investment behavior is attributed to genetics; Barnea, Cronqvist, Siegel (2010)

Nature abhores an undiversified bet (p195) [i.e.: hedge risks most effectively]

Leibowitz (2005) Alpha Hunters and Beta Grazers

J. Doyne Farmer (2002) Market force, ecology and evolution

jpoletto's review

5.0

Let me start by saying that Economics, particularly Behavior Economics is a subject that I love. It started with Freakonomics, but I think I’ve read more that ten books on the topic (full list below).

Having that said, this book is not for everybody, but it is one of the best books I’ve read about the subject ever. Not only it presents a ground-breaking hypothesis for how the markets work, but a compelling one, with real-life implications and proposals.

Economics/Behavior Economics Related booklist

- The Spider Network

- A Man for All the Markets

- Black Edge

- The Undoing Project

- Narconomics

- Misbehaving

- Who Gets What and Why

- Scarcity

- The Big Short

- Flash Boys

- Game Changer: Game Theory

- The Buy Side

- The Physics of Wall Street

- Why I Left Goldman Sachs

- Sway

- The Wisdom of the Crowds

Having that said, this book is not for everybody, but it is one of the best books I’ve read about the subject ever. Not only it presents a ground-breaking hypothesis for how the markets work, but a compelling one, with real-life implications and proposals.

Economics/Behavior Economics Related booklist

- The Spider Network

- A Man for All the Markets

- Black Edge

- The Undoing Project

- Narconomics

- Misbehaving

- Who Gets What and Why

- Scarcity

- The Big Short

- Flash Boys

- Game Changer: Game Theory

- The Buy Side

- The Physics of Wall Street

- Why I Left Goldman Sachs

- Sway

- The Wisdom of the Crowds

More...